Karan Narang

With the advent of the lifestyle hotel product in the last lodging cycle and with it going mainstream in the top 25 MSA markets in the current lodging cycle, the obvious next step for the expansion of this product type is to bring it into non-top 25 MSA markets. Lifestyle hotel product has been around in the major markets for a while but are typically positioned in the upper-upscale to luxury price range. In the current cycle, though, economics and demographics in a majority of the secondary markets entered into the sweet spot for upscale lifestyle product development and, along with the revitalization of urban cores, provide substantial demand and spending power that the lifestyle product can tap into.

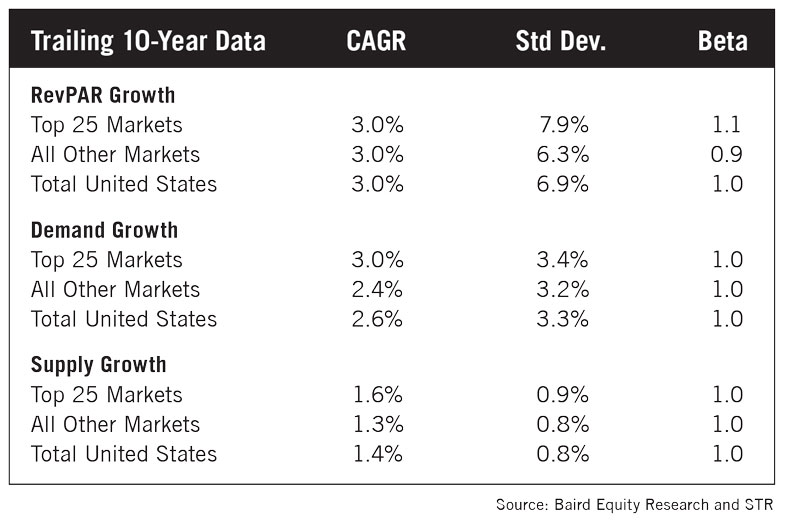

To further strengthen the case for secondary markets, a review of the trailing 10-year data presented in the chart below (Source: Baird Equity Research and STR) surprisingly shows CAGR RevPAR growth for secondary markets matching that of the top 25 markets at 3% and with a slightly lower volatility (Beta 0.9) when compared with the top 25 markets.

Per The Highland Group’s “Boutique Hotel Report 2018” and STR, lifestyle hotels constitute a mere 0.8% of hotels in smaller MSAs, with 23 out of 30 smaller MSAs having none of this hotel type. This indicates a significant opportunity for lifestyle boutique hotel development in secondary markets as consumers seek out this lodging option across all tiers.

Challenges for this product entering into secondary markets are quite a few though. A majority of the secondary markets have occupancies and ADRs that will not support a stand-alone lifestyle hotel product, especially with the current development and/or conversion costs. Per our experience, this is in spite of the fact that once the lifestyle product enters the market it will not have many, if any, true competitors and would command well above 100% RevPAR penetration to the existing competitive set.

In such a case, as ironic as it may sound, F&B, the historic loss leader in a traditional hotel, can actually help create a feasible lifestyle hotel product in secondary markets. F&B activation in lifestyle hotels can be a much bigger disruptor in the secondary market space than the traditional top 25 MSAs. A brand-driven, robust and fully activated F&B program that drives local and regional consumer awareness through a strong community connection allows the overall project to make up for the weaker RevPAR and continue to appeal to the experience-driven consumer.

One idea is to curate a roster of in-house and third-party F&B concepts and operators that can plug and play for market, location, demographics and brand selection. This allows you to suit the F&B offering to the local market while offering service consistency and a seamless guest experience.

In addition, depending on the market and concept selection, you can structure different types of arrangements with third-party F&B operators ranging from lease, management and licensing. This also helps to cater the offering based on the requirement of the developer from a return perspective.

With a laser focus on identifying and creating opportunities that optimize the development, F&B revenues can increase. Also, having an optimized meeting space allocation in such a product can help you successfully diversify across market segments.

With a laser focus on identifying and creating opportunities that optimize the development, F&B revenues can increase. Also, having an optimized meeting space allocation in such a product can help you successfully diversify across market segments.

Develop a strategy that specializes in bringing the neighborhood into your hotels via dynamic food and beverage programming. Consider developing an in-house team of experienced hoteliers dedicated to F&B activation, and to concepting and managing F&B programs at your properties that cater not only to the hotel guests, but are also positioned toward the locals. This allows you to not only generate a far bigger share of revenues through F&B, but also mitigate part of the broader occupancy and ADR trends.

An ever-shifting consumer mindset and, above all, an evolutionary shift in hospitality, demands a stronger emphasis on experience. Having an activated F&B program as part of lifestyle hotels in secondary markets—and one that showcases the individuality of the property and also resonates with the locals—will position the property for success in such markets and also, to some extent, tame the overall volatility in demand trends.

Karan Narang is the VP for acquisitions and development analysis at Dream Hotel Group, playing an integral role in the continued growth strategy and expansion of the group. Dream Hotel Group is a hotel brand and management company with a 30-year history of managing properties, and includes the Dream Hotels, Time Hotels, The Chatwal and Unscripted Hotels brands.

Let us know what you think… To comment on this opinion piece, or to voice your own opinion about pertinent industry topics, please email Editor-in-Chief Christina Trauthwein at [email protected]. We’d love to hear from you and share your point of view.