NATIONAL REPORT—While limited- and select-service properties get a lot of industry buzz due to their relative affordability, once hoteliers have found success in that segment, many often become aspirational and look to “step up” to upscale and upper-upscale hotels. Hotel Business recently turned to a variety of experts to see how these segments are faring in the current economic environment, as well as how robust the lending landscape might be for these project types.

NATIONAL REPORT—While limited- and select-service properties get a lot of industry buzz due to their relative affordability, once hoteliers have found success in that segment, many often become aspirational and look to “step up” to upscale and upper-upscale hotels. Hotel Business recently turned to a variety of experts to see how these segments are faring in the current economic environment, as well as how robust the lending landscape might be for these project types.

CEO Pablo Alonso noted proprietary data from his research company, HotStats, suggested 2017 was a very positive year for hotels in the upper-upscale segment, which he said outperformed hotels in the upscale segment.

“For upscale hotels, the main challenge has been with escalating costs outpacing mediocre increases in revenue, and, as a result, properties in this segment suffered a 2.6% year-on-year drop in profit. In contrast, growth in the upper-upscale segment was driven by stronger rooms-revenue growth, as well as increases in other revenues, and properties in this segment also did a much better job of controlling their cost base. As a result, hotels in the upper-upscale segment recorded a 2.5% year-on-year increase in profit.”

Alonso indicated this year could see more of the same, “as national minimum wage increases continue to put pressure on hotel profits and, due to a broader revenue base, upper-upscale hotels will always have more levers to pull. A focus on driving operational efficiencies from upscale operators could ensure that cost creep doesn’t continue to eat into overall profitability,” he said.

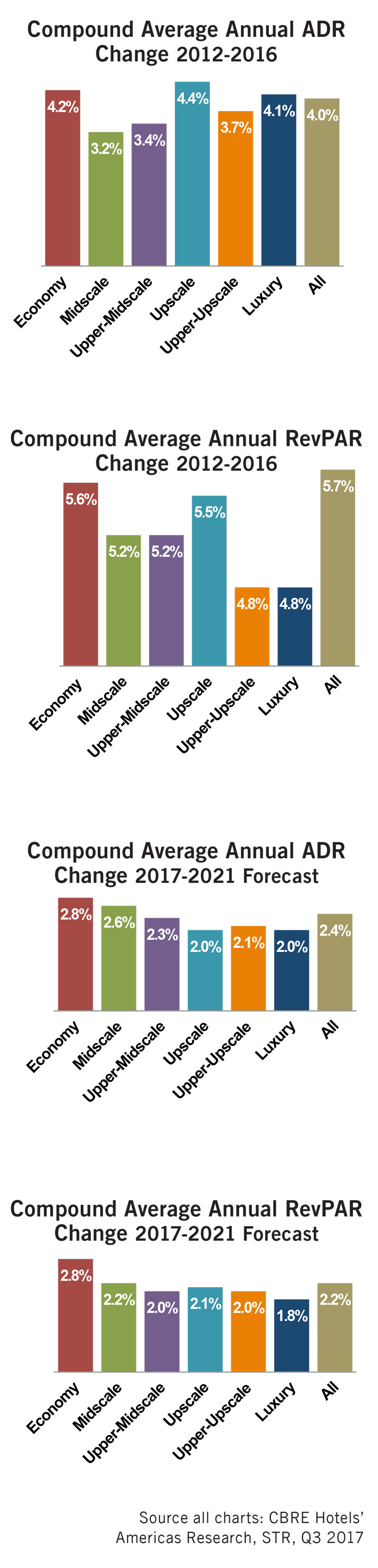

Consumers are also becoming more aspirational in their choices, which could impact the segments’ revenues. According to R. Mark Woodworth, senior managing director of CBRE Hotels’ Americas Research, its data reveals that changes in demand for upscale and upper-upscale correlates closely to changes in real personal income. “The elevated levels of economic growth, the growing ‘wealth’ effect that comes from a rising stock market, increasing home prices and, for some, the benefit that comes from bonus payments and wage hikes associated with the recently enacted tax law changes suggests these recent trends should comfortably continue in the near-to-mid-term,” he said.

PwC-Hospitality & Leisure Managing Director Warren Marr observed upper-upscale hotels had the highest occupancy level of all the chain scales in 2017, closely followed by upscale and luxury. “The resilience of the upscale chain scale segment is notable, as it had by far the largest percentage increase in supply. However, upper-upscale and upscale hotels had the lowest increases in ADR within the chain scales last year. For upper-upscale hotels, this can largely be attributed to a lack of group compression, as well as softness in corporate transient demand. For upscale hotels, it was the need to attract a more price-sensitive leisure traveler to compensate for softness in corporate demand, augmented by the significant increases in new supply within that chain scale.”

CBRE’s Director of Research Information Services Robert Mandelbaum added several convention hotels operate in the upper-upscale segment, “so performance is somewhat tied to the health of group demand” as well.

Like CBRE, PwC expects underlying macroeconomic and industry fundamentals to remain strong this year. “Supply growth in the upscale chain scale is expected to moderate, while demand growth is anticipated to continue to support record occupancy levels. Strength in consumer spending and the potential for an uptick in corporate transient demand are anticipated to drive a more meaningful uptick in ADR growth for both the upper-upscale and upscale chain scales compared to last year,” said Marr.

In terms of supply/demand growth, Patrick “JP” Ford, SVP/director of business development at Lodging Econometrics (LE), said, “Upscale should see 5% supply growth for 2017, with 5.4% expected in 2018 while upper-upscale should see 1.7% supply growth for 2017, with 2% expected in 2018.”

Supply growth is expected to remain measured with “little concern of overbuilding” in the majority of markets, noted CBRE’s Woodworth. “These two chain scales have consistently achieved occupancy premiums relative to the industry average, and these are expected to continue despite the significant volume of new development in the upscale hotels category. According to STR, demand for these property types has historically grown at almost four times the national average. Fortunately for developers, construction economics have been market supported and new supply has kept up with this demand. This is not likely to change in the foreseeable future, particularly in view of the number of new brands entering this space. A similar phenomenon is true, to a lesser degree, in the upper-upscale segment,” he said.

LE’s Ford noted upscale infiltrating urban centers, airports and shared-sites with extended-stay brands “has improved the segment’s offerings [while]upper-upscale has had a few soft brands drive growth.”

According to Elliot Eichner, principal at Sonnenblick-Eichner Co., capital is readily available for adaptive-reuse and mixed-use projects in both segments. “These are typically LIBOR-based loans and are being provided, for the most part, by debt funds, Wall Street lenders with floating-rate programs and banks. The largest amount of capital is available for permanent loans for seasoned properties,” he said.

David Sonnenblick, also a company principal, observed for those seeking a construction loan or an interim repositioning loan, “lenders will want to see a seasoned developer who has net worth and liquidity, but also experience in hotel development and repositioning. Having a good hotel management company is important in all instances.”

David Sonnenblick, also a company principal, observed for those seeking a construction loan or an interim repositioning loan, “lenders will want to see a seasoned developer who has net worth and liquidity, but also experience in hotel development and repositioning. Having a good hotel management company is important in all instances.”

Lenders are generally more cautious regarding construction loans, noted Eichner. “Lenders that will provide first-mortgage construction loans, the level typically will not exceed 65% of project cost. There are lenders, typically private debt funds, that will go higher in the capital stack for hotel-construction loans, but underwriting these deals are typically the most difficult,” he said.

Any perceived disadvantages around the segments could actually stem from the high levels of development interest in them, particularly upscale, which might suggest an elevated risk of excess supply entering the market, observed Woodworth, although CBRE sees the probability of this remaining low.

And despite the limited-/select-service juggernaut, each of the upper-level segments apparently remains appealing to owners and developers.

“Most definitely,” said HotStats’ Alonso, “But ultimately this is determined by the development dynamics of a market opportunity. In many locations, potential development options will be restricted to a product of a limited/select-service market positioning as the overall financial viability, in terms of the value created relative to the cost of delivery, is likely to be marginal. Should market dynamics allow, the premium top- and bottom-line performance of upscale and upper-upscale hotels will allow for development.”

Upscale in particular remains very attractive, according to Ford. “The brands in this chain scale have wide consumer acceptance, are relatively easy to operate, have strong reservation systems, and, as a result, are more easily financed,” he said.

“It’s important to note that some of the most successful, and profitable, select-service brands, sought out by owners and developers, are actually in the upscale segment,” said PwC’s Marr. “From a conversion perspective, the same holds true, with many buyers acquiring a hotel, putting some CapEx into it, and repositioning the hotel under a new brand within the upscale segment. Upper-upscale hotels require a lot more diligence by the buyer or developer today. In some locations, they can be extremely profitable. That said, the cost of operating food and beverage in a high-labor-cost market can be a drain on the bottom line for an upper-upscale hotel, so a strong group mix is often an essential ingredient for success.”

Overall, Eichner said the lending landscape continues to look good. “All institutional capital sources will make loans on hotels in these segments.”

“Simply said, developers of these property types are delivering what the consumer wants,” concluded CBRE’s Woodworth. HB