The upscale hotel segment’s many popular brands continue to make it the main choice for new development, leading to somewhat unfavorable demand trends in 2018. Even though the upscale segment is expected to post industry highs for demand, it will also see industry-wide highs for new supply, at levels far above any other segment.

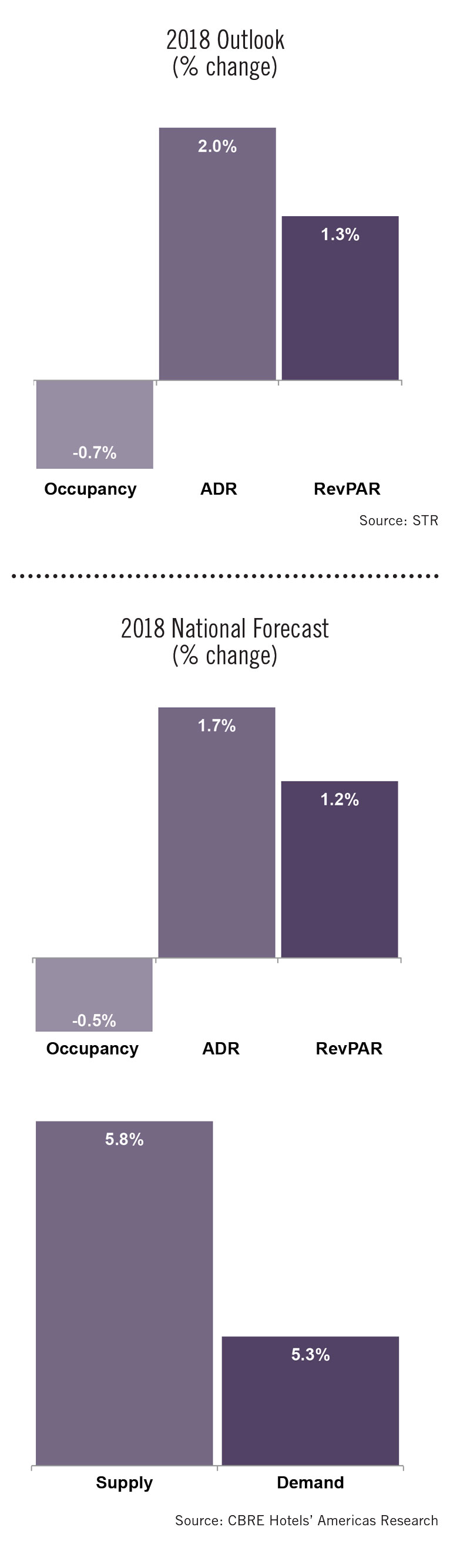

According to the latest forecast from CBRE Hotels, the upscale segment will be a strong draw for travelers in 2018, growing demand by 5.3%, well above the overall industry projection of 2% demand growth. The issue is that upscale hotels are also expected to see supply growth of 5.8%, nearly three times the industry-wide average of 2% supply growth. The only other segment experiencing even roughly similar levels is upper-midscale, which is expected to see just 2.7% supply growth in 2018.

“As far as the absolute number of construction, those upscale brands like Courtyard, Hilton Garden Inn and Homewood—plus the upper-midscale brands like Hampton and Fairfield Inn—they still account for two-thirds of what’s under construction, and that’s really going to continue to be the case as we go into 2018,” said Bobby Bowers, SVP of operations for STR. “It’s still the same types of products driving it that have been for the last four or five years.”

The impact of that new supply will primarily be seen in segment-wide occupancy declines in 2018. CBRE is expecting a minor occupancy dip of -0.5% to 72.9% overall, an ADR gain of 1.7% to $142.47 and RevPAR growth of 1.2% to $103.92. STR is projecting similar numbers for the segment, with a year-end 2018 occupancy decline of -0.4%, ADR growth of 1.5% and a RevPAR increase of 1.1%.

“Year over year, we’re forecasting that the upscale segment occupancy will decline,” said Mark Woodworth, senior managing director of CBRE Hotels’ Americas Research. “It’ll go down about a half point, which will give weaker pricing power—i.e., room rates only going up 1.7%—and a relatively weak 1.2% RevPAR change. It’s because we’ve got a lot of new rooms, most of which are going to be absorbed, but, in part, at the expense of lower room rates. Pricing power will be impaired in most markets if you’re an upscale hotel.”

“Year over year, we’re forecasting that the upscale segment occupancy will decline,” said Mark Woodworth, senior managing director of CBRE Hotels’ Americas Research. “It’ll go down about a half point, which will give weaker pricing power—i.e., room rates only going up 1.7%—and a relatively weak 1.2% RevPAR change. It’s because we’ve got a lot of new rooms, most of which are going to be absorbed, but, in part, at the expense of lower room rates. Pricing power will be impaired in most markets if you’re an upscale hotel.”

Upscale hoteliers tend to agree, especially after seeing 6% supply growth in 2017. Sources told Hotel Business that what’s even more troubling is the concentration of new upscale supply in the top national markets. It creates a situation where even though the overall national trends remain positive for the segment, specific geographic areas may be experiencing a more disproportionate supply-demand relationship.

“The problem in upscale is that much of the supply addition has been concentrated in that area, and the supply that has been added seems like it’s all been added in the top 25 markets—urban and high-suburban Hilton and Marriott brands,” said Brian Fry, president of Commonwealth Hotels LLC. “We look at the national projections and they look pretty good—a couple of points and you’re going to be all right—but if you look at the upscale class broken out, it’s significantly less. We think it’s going to be a little challenging there.”

That hasn’t stopped hoteliers from planning new development in the segment. According to Chris Diffley, managing director of Rockbridge Capital, there are still opportunities for new product on a market-by-market basis.

“Not all markets are created equal,” said Diffley. “We’re not shying away from new development. We’re opening assets in Seattle, New Orleans and Savannah, GA, in 2018. We’ve recently opened assets in Nashville, TN, and we opened an asset in 2017 in San Jose, CA. The demand and growth dynamics of some of those markets merit new supply.”

Experts remain confident that the seemingly unshakeable strength of the upscale hotel brands—which include many of the newer lifestyle, boutique and select-service flags—continues to foster demand that’s robust enough to mitigate much of the downside from new supply in 2018. With a projected occupancy still hovering near 73% for all upscale hotels, developers will continue to seek opportunities in the segment.

“There are a lot of nice, clean, crisp concepts that have been brought to the market over the past two to five years that are really targeting that traveler who wants something new and fresh, but doesn’t have an unlimited budget,” said Woodworth. “That explains why developers are still really focused on that upscale category.”