Industry pundits expect midscale hotels to post modest 2018 gains in ADR and RevPAR, and either a slight dip or a small boost in occupancy, depending on who you ask. Sources say the lack of new product in the segment, paired with the popularity of upper-midscale hotels, has resulted in minimal demand growth for the chain scale.

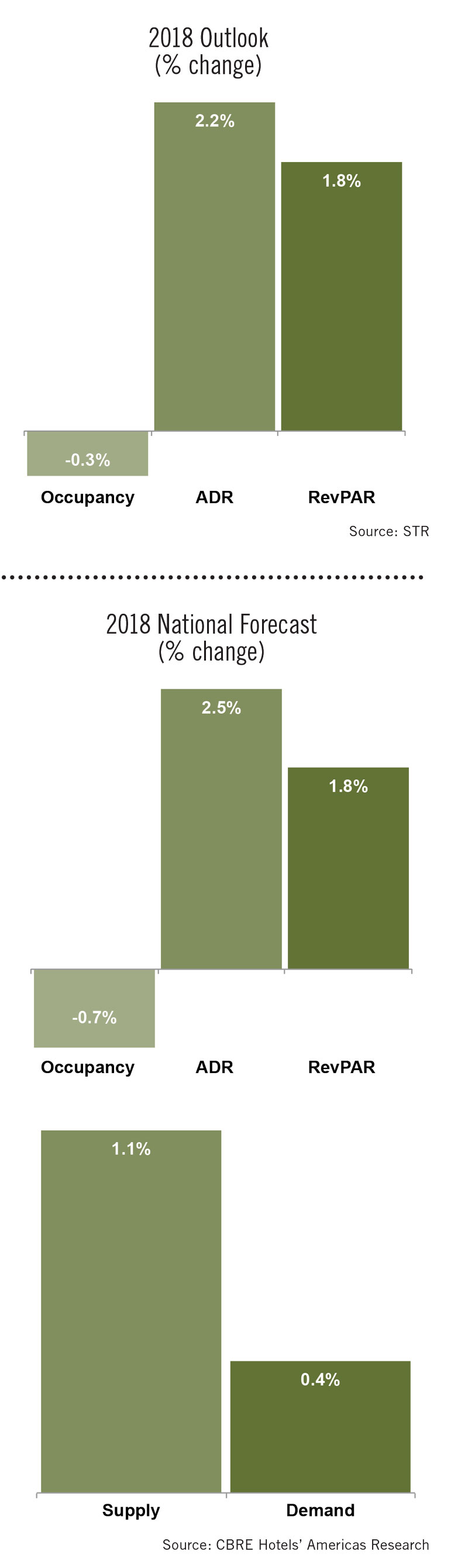

Although CBRE Hotels is forecasting midscale supply to increase just 1.1% in 2018, that new supply still outpaces demand growth, which is projected at just 0.4% for the year. Sources say this is mostly the same old story for the segment, which has posted occupancies hovering just below 60% in recent years.

“Despite record occupancy levels in the industry, these hotels remain below 60%,” said Robert Mandelbaum, director of research information services for CBRE Hotels’ Americas Research. “It speaks to the demand for those types of accommodations.”

The firm predicts that trend will continue. CBRE is expecting a minor midscale occupancy dip of -0.7% to 59.4% overall, an ADR gain of 2.5% to $89.17 and RevPAR growth of 1.8% to $52.98. STR is projecting somewhat more optimistic numbers for the segment, with a year-end 2018 occupancy increase of 0.9%, ADR growth of 2.1% and a RevPAR increase of 3.1%. Sources told Hotel Business that the chain scale doesn’t presently have much leeway for pushing either rate or occupancy, partly due to outdated product.

“Midscale is one of the two lowest occupancy chain scales out of all the STR chain scales, so right away, you begin to question what kind of pricing power they might have,” said Mark Woodworth, senior managing director of CBRE Hotels’ Americas Research. “This is where you see a lot of conversion-type activity of older properties moving into this segment. We do believe that new beats old every time, and you don’t see as much construction activity here, so that hurts midscale in terms of being able to run higher occupancies on an annualized basis. As a result, generally speaking, their pricing power’s not quite as good.”

“Midscale is one of the two lowest occupancy chain scales out of all the STR chain scales, so right away, you begin to question what kind of pricing power they might have,” said Mark Woodworth, senior managing director of CBRE Hotels’ Americas Research. “This is where you see a lot of conversion-type activity of older properties moving into this segment. We do believe that new beats old every time, and you don’t see as much construction activity here, so that hurts midscale in terms of being able to run higher occupancies on an annualized basis. As a result, generally speaking, their pricing power’s not quite as good.”

Midscale’s pricing power is also hampered by the ubiquity of popular select-service brands that comprise the upper-midscale and upscale segments. Those two chain scales have seen and continue to exhibit considerable supply growth, impacting the players in the pricing tiers both above and below them.

“Midscale is still impacted by the growth in rooms supply in the other segments,” explained Jerome F. Cataldo, president and CEO of Hostmark Hospitality Group. “There’s a lot of select-service rooms coming on in lots of markets, and I think it affects all of those categories in midscale and up. Even though the supply growth maybe isn’t as significant directly in midscale, I still think midscale is affected by the supply growth in those other segments.”

Still, with projected occupancies for the segment remaining at a similar level as 2017’s 59.9% occupancy—the chain scale’s best occupancy performance in recent history—operators are confident in another strong year. There appears to be room to continue to boost room rates, even if on a relative basis that means an increase of just a few dollars per room night.

“We are primarily focused on driving rates in 2018, since we are already experiencing historic occupancy levels,” said Greg Friedman, CEO of Peachtree Hotel Group. “With a strong economy, businesses are willing to spend money to get out and do business again, while leisure guests are taking advantage of the prevailing financial outlook to get back on the road to explore.”

That doesn’t mean, however, that developing new product in the segment will get any easier in 2018. According to experts, the lending climate still remains tricky for midscale projects, with much of the development capital continuing to flow into the upscale and upper-midscale segments instead. CBRE expects new supply in the segment to remain around 1% for the foreseeable future.

“The lending and development environment remains challenging on multiple fronts,” said Friedman. “The regulatory pressures, coupled with concerns that we are approaching the end of this economic cycle, have caused traditional hotel lenders and banks to remain conservative. Most banks today are lending at 50-65% of the total project cost, which is a lower leverage point than was achieved in previous cycles. It has been tough to make new-development projects pencil, with rising construction costs and the challenges on the lending side.”