NATIONAL REPORT—Will the good times continue to roll in 2019? While there are factors that could affect the performance of the industry, all signs point to a good—but not great—year for the hotel industry.

“At the macro level, the industry continues to perform very well,” said Mark Woodworth, senior managing director of CBRE Hotels’ Americas Research. “One of the ways we describe the current cycle is we’re now at that point where we’re performing at peak levels, certainly in terms of occupancy, and going forward, that performance, we think, will be very durable.”

What does “durable” mean exactly? Woodworth explained, “We think about some critical things as it relates to impacting the performance of hotels—certainly, the economy and economic conditions and what that means in terms of changes in demand for hotel rooms, consumers’ willingness in terms of price, etc.; then there’s where we are in the property cycle, meaning how is supply changing and will there be enough new demand to support the new supply and what might that do to industry fundamentals?

“The answer to all of the above is a very balanced supply-and-demand relationship as far forward as we can see,” he continued. “We feel confident the economy, which has been good in 2018, will still be good comfortably into 2019 and well into 2020, such that owners and operators, as they think about the year ahead, should feel very good that it’s going to be, at the macro level, another year of good—but not great—growth and another good year for hotel profits.”

“The answer to all of the above is a very balanced supply-and-demand relationship as far forward as we can see,” he continued. “We feel confident the economy, which has been good in 2018, will still be good comfortably into 2019 and well into 2020, such that owners and operators, as they think about the year ahead, should feel very good that it’s going to be, at the macro level, another year of good—but not great—growth and another good year for hotel profits.”

Bobby Bowers, SVP of operations for STR, noted that Tourism Economics, the company that does the economic modeling for STR’s forecasts, sees growth in real gross domestic product slowing a bit in 2019. “Their forecast for full-year 2018 is 2.9% and then 2019 is 2.5%,” he said. “A little bit of that is due to the short-term boost in the tax reform, and that’s going to be gone in 2019. From the perspective of how that affects lodging, what we have forecast for 2019 for the industry as a whole is a little slowdown of demand—it’s still healthy at 2%, but we’re seeing supply growth will be about the same, so overall, we’re looking for occupancy rates in 2019 for the industry as a whole to be kind of flat. Rate growth will drop a bit, so RevPAR growth will be about 2.4% for the whole year of 2019, which would be down… Our forecast for 2018 is about 3% growth, so it would be down a bit from the year as we expect to see it end in 2018.

“If you look at RevPAR growth, and you look at it on a 12-month moving average, we’ve had growth in RevPAR for more than eight years, so it’s a really long time we’ve had this growth,” Bowers said. “For 2019, we’re seeing kind of the same type of environment that we’ve had in 2018, just a little bit slower.”

Overall, both CBRE and STR are projecting a 1.9% increase in supply. According to J.P. Ford, SVP and director of business development, Lodging Econometrics, “Overall, the horizon looks good for the continuation of the current hotel lodging cycle into 2019. Compared to where we are today, I expect more of the same heading into 2019, especially in the first half of the year. From a supply standpoint, the U.S. construction pipeline is growing, albeit at a decelerating pace, but still continued growth quarter over quarter in terms of number of projects and the number of rooms. We’re seeing a pretty healthy influx of new projects in the early planning stage as well, so that bodes well for the pipeline moving forward in 2019. Our forecast for new hotel openings we expect will be rather strong in 2019 and 2020, based on what’s in the pipeline already.

“We’re in pretty healthy economic times at the moment,” Ford reflected. “We have consumers with more discretionary income today, people enjoy traveling, corporate profits are pretty good, so you’ll have a lot of corporate travel as well. When you look at all of those factors, it bodes well for the hospitality industry. Planes are still jammed full, there are very few seats available. There’s a lot of people out on the road traveling. I’m rather positive on where we’re headed into 2019.”

That being said, there are a variety of macroeconomic factors the experts are keeping their eye on that could affect the year ahead.

Trouble brewing?

For Bowers part, he sees interest rates and tariffs as two main issues hoteliers are concerned with. “This is probably something that’s got the markets spooked—the fact that interest rates will continue to go up, and people are unsure about how that will affect things. We continue to have worries and concerns about how the tariffs and trade war might affect the economy in general. Those are the two things that stand out,” he said.

Ford agreed, adding, “The continued rise in interest rates can be bothersome and worrisome for many people. Also, keeping an eye on the effect of the tariffs, and how that will impact our industry going forward. Hopefully, there’s some sort of settlement that might be able to be reached, but I’ve got my eye on that as well.”

“From a construction, supply-growth standpoint, we’ve seen under-construction rooms, for the most part over the past nine or 10 months, slow down a bit, and with hurricanes in Florida and North Carolina and the fires in California, that could present a strain on not only construction materials, but labor,” Bowers said. “If you think about all of that stuff put together, from a supply standpoint, on the hotel side of things, it might tend to make supply growth slow down a bit, which wouldn’t be a totally bad thing.”

“There are five markets with very strong pipelines: New York, Dallas, Houston, Los Angeles and Nashville, TN,” Ford said. If you’re a current owner or developer looking at one of those markets, you need to be attuned to that. If you’re an owner thinking about what operational adjustments you need to make based on new competition down the road or around the block, you need to be attuned to that. If you’re a developer, you have to be looking at whether there’s enough space or enough demand in this market that will absorb the extra supply they’ll be bringing with those projects.”

Looking at potential concerns, Woodworth added, “It’s almost like, what day is it and what should we be concerned about?” Issues that could affect hospitality are numerous: political instability in Washington, how Brexit will play out, the price of gas, volatility in the public markets, tariffs, and what the Federal Reserve plans to do, to name a few.

“It’s a lengthy list of issues, but the good news is, in a sense, there’s things that can make you optimistic about continued if not greater levels of economic growth,” Woodworth said. “At the same time, there’s perhaps offsetting issues that we’ll finally begin to slow down somewhat, but overall, our house view continues to be that 2019 should be a good year of economic growth, and inflation will stay in check; the positive residual benefits from the tax cuts enacted at the beginning of this year are now expected to last longer, well into 2019, so that will help the economy, which will help the demand for hotel rooms. There’s a lot of noise in there, and as we try to look through that, understand what the pros and cons of some of these issues are, our own view is the net should be another good, favorable year for hotel demand and, therefore, the industry.”

Rate issues

One industry question many have been trying to answer is the problem with rates. Overall for the industry, rate is expected to grow in 2019—CBRE pegs it at 2.5% growth to $133.15, while STR sees 2.3% growth—but with occupancies at record numbers, one question everyone asks is why aren’t rates growing faster, Bowers said.

“Occupancies have really been—and really still are—pretty high, especially at the top end; if you look at luxury, upper-upscale, and upscale occupancy, it’s hard to grow them a whole lot more,” he said, noting he thinks the inability to grow rate is based on a combination of factors. “With online travel agencies and all of the information you have available via the internet, in terms of price transparency, that’s had some effect on the ability to increase rates. It’s also alternative accommodations like Airbnb in certain markets like New York and San Francisco. It’s also partly due to the fact that inflation has been really low for a long time and it’s been hard to pass along any kind of cost increases to the consumer. I’m not an economist, but if interest rates are starting to go up a bit, you look at companies beginning to be able to push a bit more increases in price along. We may be able to see a little more growth than we saw in 2018; I just don’t think it will be huge.”

For his part, Woodworth said, “As I think about our forecast in recent years, including 2018, the two areas we have missed most consistently—fortunately, not by a lot, but we’ve missed it—is room rates have not increased at the level one would expect them to given what we can learn from studying history. These high occupancies should be giving greater pricing power, but it’s not filling up the numbers, so ADR growth has been weaker than history would have said it should have been; conversely, demand growth has consistently been higher than what we expected it to be given history and the performance of the economy. In some respects, when we do this estimating, we continue to be in a mode where going forward we’re very comfortable with the level of demand growth that we’re forecasting, but if we’re wrong, I continue to believe it’ll be a bit better than we’re saying. Similarly, where once again even though we think U.S. hotels will achieve all-time high record occupancy in 2019, we’re still expecting relatively weak increases in average daily room rates because there’s no evidence yet to suggest whatever has been undermining pricing power for hoteliers, it’s begun to dissipate at all.”

Robert Mandelbaum, director of research information services, CBRE Hotels’ Americas Research, added that he was recently with a group of sales and marketing managers and “they constantly kept bringing up all these new hotels under construction, and I think that’s maybe impacting how they’re approaching pricing.”

“That’s not surprising because we know from studying history when you add rooms to a market, it makes a difference,” Woodworth said. “And usually that difference is not positive in nature.”

“One of the things we talk about is what are some of the things that could potentially cause the next downturn, and we have enough grey hair to remember the times that it was oversupply that caused downturns of the industry,” Mandelbaum said. “I’m looking at segments where there’s still a lot of growth going on—upper-midscale [is projected to have]3.5% change in supply next year, 4.7% to the upscale sector, yet we’re still forecasting growth in occupancy in both sectors, so that emphasizes the underpinning that the economy is there to support demand that’s even filling up the new hotel rooms that are being built.”

Overall health

Looking at the 2019 forecast, STR projects a 1.9% increase in supply, 2% increase in demand, 0.1% increase in occupancy, 2.3% increase in ADR, and 2.4% increase in RevPAR for the industry overall.

For its part, CBRE projects similar numbers: a 1.9% increase in supply, 2.1% increase in demand, 0.1% increase in occupancy to 66.2%, 2.5% increase in ADR to $133.15, and a 2.7% increase in RevPAR to $88.11.

“As we think about 2019, in some ways, it could very well be a repeat of 2018, meaning the stronger chain scales, and we’ll define that as being the greatest RevPAR growth, are a barbell view—luxury should be very good, above the national average RevPAR growth, while we expect the strongest segment will be economy hotels,” Woodworth said. “Our RevPAR for luxury is 3%. All hotels is 2.7% and economy is 3.7%. Part of the rationale behind that is on the high end, there will be some level of supply growth, but what’s really driving it is that income levels, profit levels will be strong again in 2019, and those are the economic variables that correlate most closely to the demand in high-end hotels.

“The factor driving economy and midscale next year, in part, is unlike almost all other chain scales; they have the capacity to grow, meaning their occupancies are significantly lower than what we see at the high end,” Woodworth said. “Fundamentally, if my hotel is sold out, I can’t accommodate any more business. The opportunity to grow revenues is strictly by increases in room rate, and we’ve seen a lot of evidence for the last few years that has been a very difficult challenge. I’m capping out on the occupancy side the higher up the chain scale I go, but on the low end, we’re still well below the national average and we’ve got excess capacity that we think will get occupied next year.”

“And, in those two segments, there’s also the least change in supply,” Mandelbaum added. “In fact, we’re projecting a decline in the inventory of economy rooms; it’s the segment where people are either closing out of or converting out of. They have the benefit of whatever level of economy and midscale demand there is, there’s not a lot of competition. That also allows occupancy to increase.”

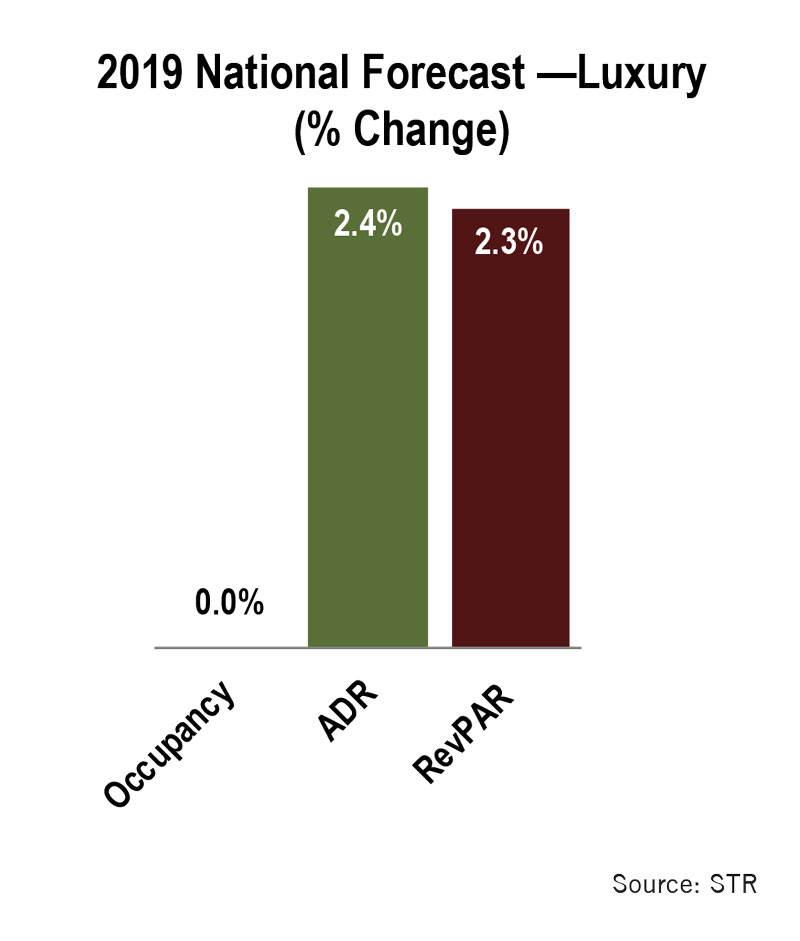

Luxury

In 2019, STR projects luxury occupancy to be flat, and a 2.4% increase in ADR, resulting in a 2.3% RevPAR increase. CBRE sees flat occupancy at 74.6%, a 3% increase in ADR to $345.48, a 3% increase in RevPAR to $257.59 and 2.7% growth in supply and demand.

In 2019, STR projects luxury occupancy to be flat, and a 2.4% increase in ADR, resulting in a 2.3% RevPAR increase. CBRE sees flat occupancy at 74.6%, a 3% increase in ADR to $345.48, a 3% increase in RevPAR to $257.59 and 2.7% growth in supply and demand.

“Higher income travelers supported by either corporations or personal wealth has maintained itself, and so the traditional guest who stays in luxury hotels, their economic means have been maintained and grown, and so the demand is there for those hotels,” Mandelbaum said.

“Luxury, in 2018 especially, they’ve really benefited from the general economy—the wealth effect and the markets have done well up until the past month or so,” Bowers said, adding that he expects that to continue.

Echoing Woodworth’s point about occupancy, he added, “There probably won’t be as much occupancy growth from them because the occupancies are so high now, but we’re expecting them to continue to do well in 2019.”

According to Lodging Econometrics, there are 29,700 luxury rooms in the construction pipeline, representing 5% of the total U.S. pipeline.

“From the standpoint of new supply, those projects are the hardest to do because only certain markets can support them, they’re expensive to do—there’s a lot of risk,” Bowers added.

Mandelbaum added, “Moderating changes in supply is the high cost of construction labor. From an operational standpoint, the cost of building a hotel has increased significantly. We hear our clients talking about how they got bids from construction companies and four months later it’s increased 20%. Or workers are abandoning sites and going to the latest hurricane-hit place and getting paid twice as much. That, too, is pressing supply growth, and you feel it more at high-end properties, where it’s a higher level of amenities and services that have to be built out and offered.”

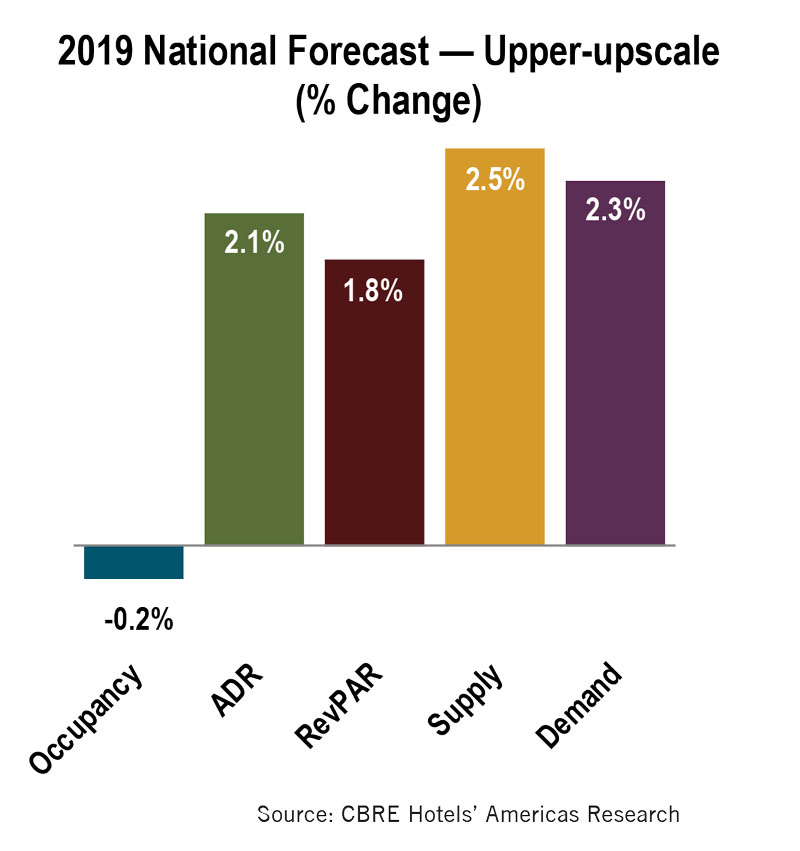

Upper-upscale

In 2019, STR projects upper-upscale to see a 0.1% decrease in occupancy, 2.3% increase in ADR, resulting in a 2.1% increase in RevPAR. CBRE projects a 0.2% decrease in occupancy to 74%, 2.1% increase in ADR to $190.13, 1.8% increase in RevPAR to $140.71, a 2.5% increase in supply and a 2.3% increase in demand. According to Lodging Econometrics, there are 74,906 upper-upscale rooms in the pipeline, 12% of the total U.S. construction pipeline.

In 2019, STR projects upper-upscale to see a 0.1% decrease in occupancy, 2.3% increase in ADR, resulting in a 2.1% increase in RevPAR. CBRE projects a 0.2% decrease in occupancy to 74%, 2.1% increase in ADR to $190.13, 1.8% increase in RevPAR to $140.71, a 2.5% increase in supply and a 2.3% increase in demand. According to Lodging Econometrics, there are 74,906 upper-upscale rooms in the pipeline, 12% of the total U.S. construction pipeline.

“There’s been a bit of an increase in [construction],” commented Bowers. “We’ve got 26,500 under construction now in that upper-upscale group, and out of all of the chain scale groups, that’s the third-highest total in the number of rooms under construction. There’s been a bit of an uptick there in construction activity in that group.”

That being said, Mandelbaum noted, “If you talk to meeting planners, there’s not a lot of huge hotels being built, 600-, 700-, 1,000-room hotels with big meeting space, and I know meeting planner surveys are concerned because their potential inventory of hotels to select from is fairly limited despite moderate near long term average pace of supply growth. A lot of hotels being built can’t accommodate those meetings, and it is a challenge for them, so that does give the upper-upscale properties some leverage because there’s not as much big-box competition.”

“From a development standpoint, even though the industry is prosperous, there still is a relatively conservative lending environment out there, which has helped moderate the level of new supply coming out of the last industry recession, so that’s why we’ve reached long run average in terms of change in supply, but we haven’t exceeded,” he added. “Getting funding for a 900-room hotel without any public assistance is a challenge.”

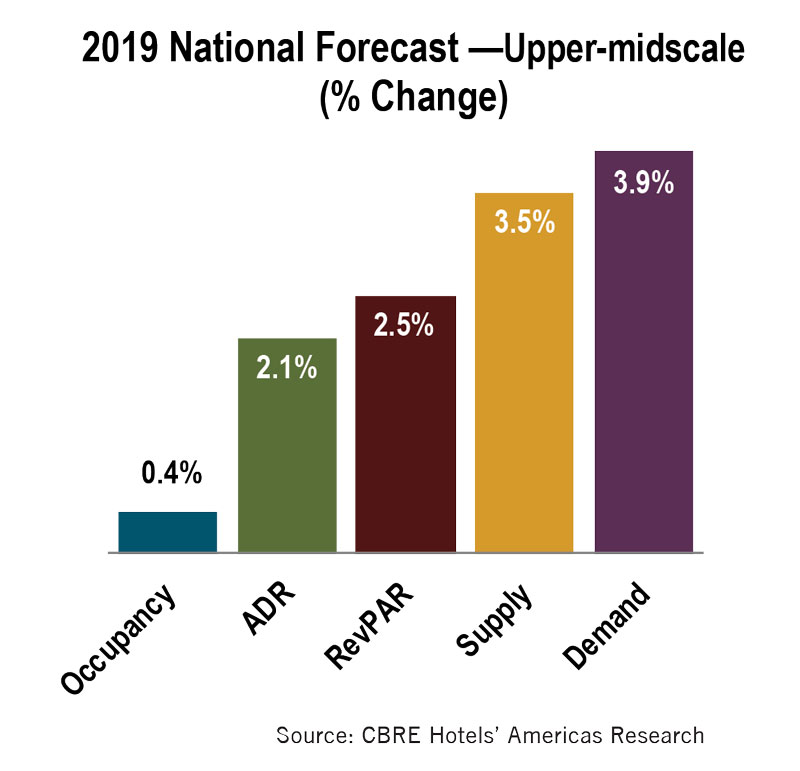

Upscale/Upper-midscale

While both upscale and upper-midscale are their own distinct segments, the trends in both are expected to be similar next year. For instance, in 2019, STR projects upscale occupancy to decrease by 0.2% and ADR to increase by 2.1%, resulting in a 1.9% increase in RevPAR. By comparison, STR projects upper-midscale occupancy to decrease by 0.1%, ADR to increase by 2% and RevPAR to increase by 1.9%.

While both upscale and upper-midscale are their own distinct segments, the trends in both are expected to be similar next year. For instance, in 2019, STR projects upscale occupancy to decrease by 0.2% and ADR to increase by 2.1%, resulting in a 1.9% increase in RevPAR. By comparison, STR projects upper-midscale occupancy to decrease by 0.1%, ADR to increase by 2% and RevPAR to increase by 1.9%.

For its part, CBRE is slightly more optimistic for the segments, particularly as it pertains to occupancy. In 2019, it expects upscale occupancy to increase 0.4% to 73.9%, ADR to increase 2.3% to $146.31, RevPAR to increase 2.6% to $108.05, supply to increase 4.7% and demand to increase 5.1%. With regard to upper-midscale, CBRE also projects a 0.4% increase in occupancy (for this segment, to 68%), 2.1% increase in ADR to $117.24, 2.5% increase in RevPAR to $79.68, 3.5% increase in supply and 3.9% increase in demand.

According to Lodging Econometrics, there are 217,769 upscale rooms and 230,279 upper-midscale rooms in the U.S. construction pipeline, accounting for 68% of the total pipeline.

According to Lodging Econometrics, there are 217,769 upscale rooms and 230,279 upper-midscale rooms in the U.S. construction pipeline, accounting for 68% of the total pipeline.

“Throughout this current cycle there are two main chain scales that have dominated new hotel development: upscale and upper-midscale,” Ford said. “Those have been the dominant chain scales, followed by midscale after that. It’s just been that way; I expect that to continue as I don’t see that changing drastically. There’s very little development at the luxury level, there’s little development at the economy level, and it really is in the upscale and upper-midscale.”

Why is that? “When you look at some of the brands in the upscale and upper-midscale, and you think about why are those brands so popular today, a couple of things resonate with me,” Ford said. “Those projects can be built rather quickly, they’re easy to operate, most of them have very limited food and beverage, they’re financeable—banks will lend on them—there’s wide consumer acceptance with travelers and many of those brands in those segments have strong reservation systems, which makes them rather attractive to developers.”

“It has popularity not only on the development side, with lenders and developers, but on the demand side, too,” Mandelbaum added. “Clearly, there’s a high acceptance of travelers of the new boutique lifestyle select-service brands that are entering this upper-midscale, upscale segment of the market. Those two segments have seen the greatest change in supply for the past 5-10 years, and have still maintained or grown in terms of occupancy.”

“By far, in percentage terms, the biggest supply growth we see is in the upscale category, so at the local level, if you have new rooms coming in, one thing you need to be focused on: the nature of the product, how it’s likely to compete with me given who I am, where I’m located, relative to my customer base and where the new property is coming in at,” Woodworth said, adding that while he’s optimistic about the economy, if there is a hiccup, “consumers start trading up or down in their lodging, and we tend to see most of that happen between the upscale and upper-upscale property types, so we could see a bit of that.”

“Those two groups are over 60% of what’s under construction,” Bowers said. “For the past few years, and then going into next year, it will be the same thing. They’ve really dominated the construction scene. The good part about that is looking at supply growth for them, in 2017, upscale supply was up 6%. Upper-mid was up 3.2% and we’re forecasting in 2018 for the full year and in 2019, they would be right at the leaders in terms of supply growth there. For 2019, for those two, we’re talking occupancy flat to down, because with all of the supply growth there, demand growth is still good, but it’s a little short of what the supply growth is, so occupancies will fall a bit.”

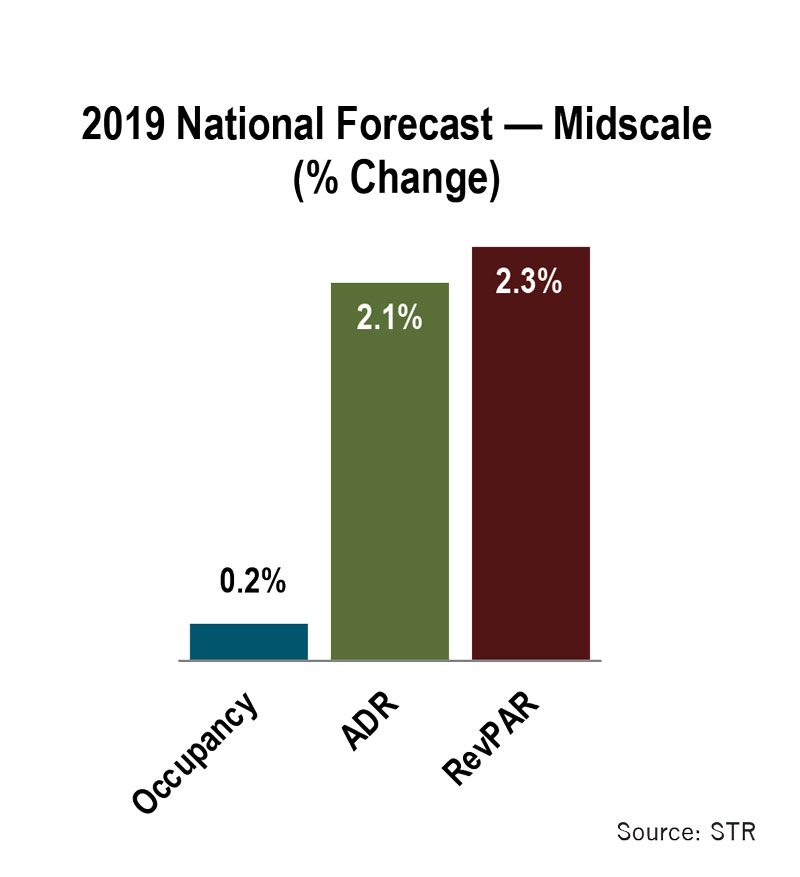

Midscale

In 2019, STR projects midscale occupancy will increase by 0.2%, ADR to increase by 2.1% and RevPAR to increase by 2.3%. CBRE sees a 0.4% increase in occupancy to 60.2%, 2.8% increase in ADR to $91.23, 3.2% increase in RevPAR to $54.92, supply increase of 0.9% and a 1.3% increase in demand. According to Lodging Econometrics, there are 77,441 midscale rooms in the U.S construction pipeline, accounting for 12% of the total.

In 2019, STR projects midscale occupancy will increase by 0.2%, ADR to increase by 2.1% and RevPAR to increase by 2.3%. CBRE sees a 0.4% increase in occupancy to 60.2%, 2.8% increase in ADR to $91.23, 3.2% increase in RevPAR to $54.92, supply increase of 0.9% and a 1.3% increase in demand. According to Lodging Econometrics, there are 77,441 midscale rooms in the U.S construction pipeline, accounting for 12% of the total.

“As I think about the more well-known midscale brands, they’re not totally, but they’re almost exclusively, conversion brands,” Woodworth said. “There’s not a lot of new development, so in conversion, often times, that owner is investing a lot of capital to be able to satisfy the standards of whatever brand they’re converting into—Red Lion, La Quinta, Best Western, etc., so I think that’s what’s driving the supply change in that particular segment; my guess, my expectation would be that like economy, a lot of that growth we expect to see in the midscale tier is going to come simply because they have the capacity to accommodate that.”

But Bowers said, the midscale category has “some of the newer brands like Tru by Hilton—there’s a lot of construction from that brand in particular. We’ll start to see a bit of that come in there.”

Economy

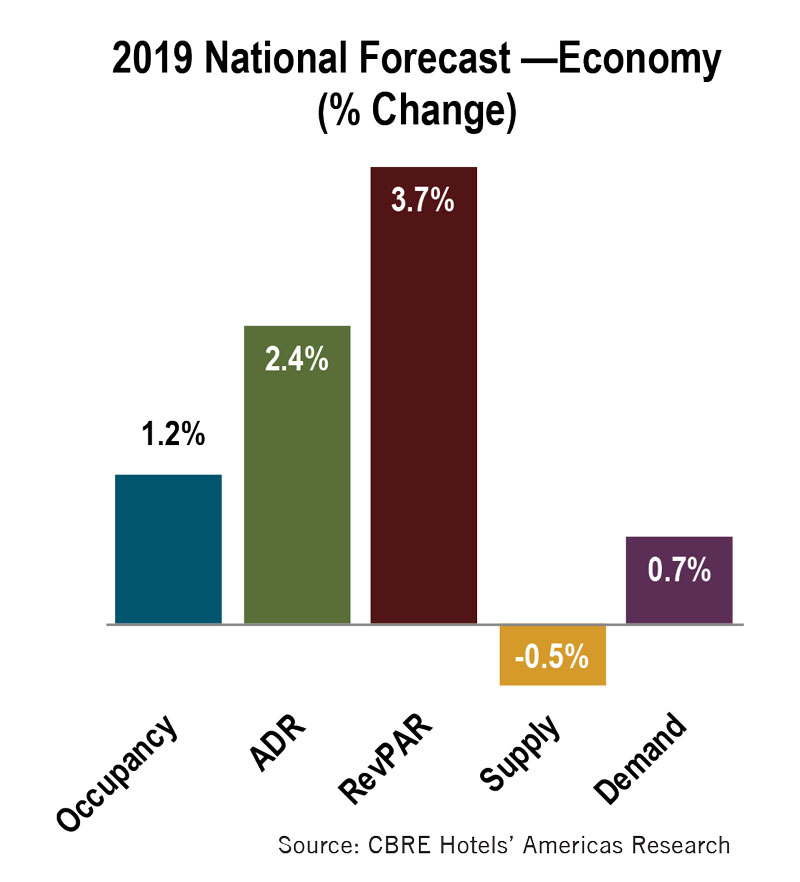

In 2019, STR projects the economy segment to see a 0.1% increase in occupancy, a 2.1% increase in ADR and a 2.2% increase in RevPAR. CBRE projects a 1.2% increase in occupancy to 58.9%, 2.4% increase in ADR to $65.44, 3.7% increase in RevPAR to $38.54, a 0.5% decrease in supply and a 0.7% increase in demand. According to Lodging Econometrics, there are 11,255 rooms in the U.S. construction pipeline, accounting for just 2% of the overall pipeline.

In 2019, STR projects the economy segment to see a 0.1% increase in occupancy, a 2.1% increase in ADR and a 2.2% increase in RevPAR. CBRE projects a 1.2% increase in occupancy to 58.9%, 2.4% increase in ADR to $65.44, 3.7% increase in RevPAR to $38.54, a 0.5% decrease in supply and a 0.7% increase in demand. According to Lodging Econometrics, there are 11,255 rooms in the U.S. construction pipeline, accounting for just 2% of the overall pipeline.

“Economy, there’s not much happening there in terms of new construction,” Bowers said. “If you look at the WoodSpring brand and Microtel, you’re seeing a little construction, but there’s not a whole lot of new construction. We’re forecasting RevPAR growth for that segment at 2.2%. Most of that is from rate, and supply growth is ticking up a bit at 0.6%. If that comes to pass, that’s going to be the biggest supply growth they’ve had in a while.”

“It’s not a recent trend, but if you look at long run averages from 1988-2017, the economy and midscale segments have the lowest occupancy levels; they’re the only two below national long run averages, where all the others are above that long-run average,” Mandelbaum said.

“In essence, why they are, from an occupancy perspective, underperforming everyone else [is because]oftentimes, even though they remain affiliated with some recognizable brand, often they’re tired, not as well maintained, and they’re old,” Woodworth said. “One thing that comes with age is not just the physical plant wears out, but many times, markets move away from the property. New growth and development of the generators of lodging supply are evolving all the time, so you may have a hotel built in the 1960s and 1970s that was in an A-plus location, but over that time frame, new roads have been built, commercial centers have evolved, and they’re no longer in or even near the heartbeat of what’s happening. As an owner, there’s not a whole lot I can do about that if the customer base is moving away from me.”

Positive vibes

Overall, the experts are optimistic about the future. “It’s one of those longer extended periods of prosperity in the industry,” Mandelbaum said. “We’re seeing all sorts of reasons for sustained revenue growth at modest levels, and if you look at the forecasts, they’re in line in terms of revenue growth—1-3% over the next few years. Therefore, the big issue right now is expenses—can you control your expenses to something less than that in order to achieve growth and profits? First and foremost, expenses with hotels is labor, and we all know the pressure on labor costs because of the low unemployment levels. That is more of a challenge for the higher chain scales because they’re more labor intensive.”

“You never know what will happen in terms of unforeseen events, but it’s almost like a replay of 2018, just a bit on the notch or two down,” Bowers added. “You start to think about it: RevPAR growth, we’re over eight years, and from 1992-2001, we had a nine-year run, so in terms of length of the cycle, we’re starting to get back to the longest we’ve tracked. It makes you think what’s going to happen? There will be some markets—San Francisco, Atlanta—that will be stronger, and some, like Houston, because of the comps and the supply growth, that won’t be as good, so it’s really a mixed bag in terms of the markets.” HB