NEW YORK—What does this year hold for hoteliers? While many in the industry saw tepid growth in the latter half of 2016—which most attribute at least in part to election-year uncertainty—new data from TravelClick indicates 2017 is off to a positive start.

“We’ve definitely seen a rebound in pace,” said John Hach, TravelClick’s senior industry analyst. “Prior to the election, there were actually five months of consecutive decline where new reservation pace had turned slightly negative. Shortly after the November election in the United States, we did see a pickup of new reservation pace.” He noted that this uptick isn’t monumental—where it had been trending down -1.5-2%, it’s now up about 1%—but even that is an improvement. In addition, said Hach, in looking at the reservation demand for the next 365 days “we’re fairly optimistic about the months of April and May. There has been a noticeable pickup in reservation activity as we start to think about the summer 2017 travel-planning season.”

John Hach, TravelClick

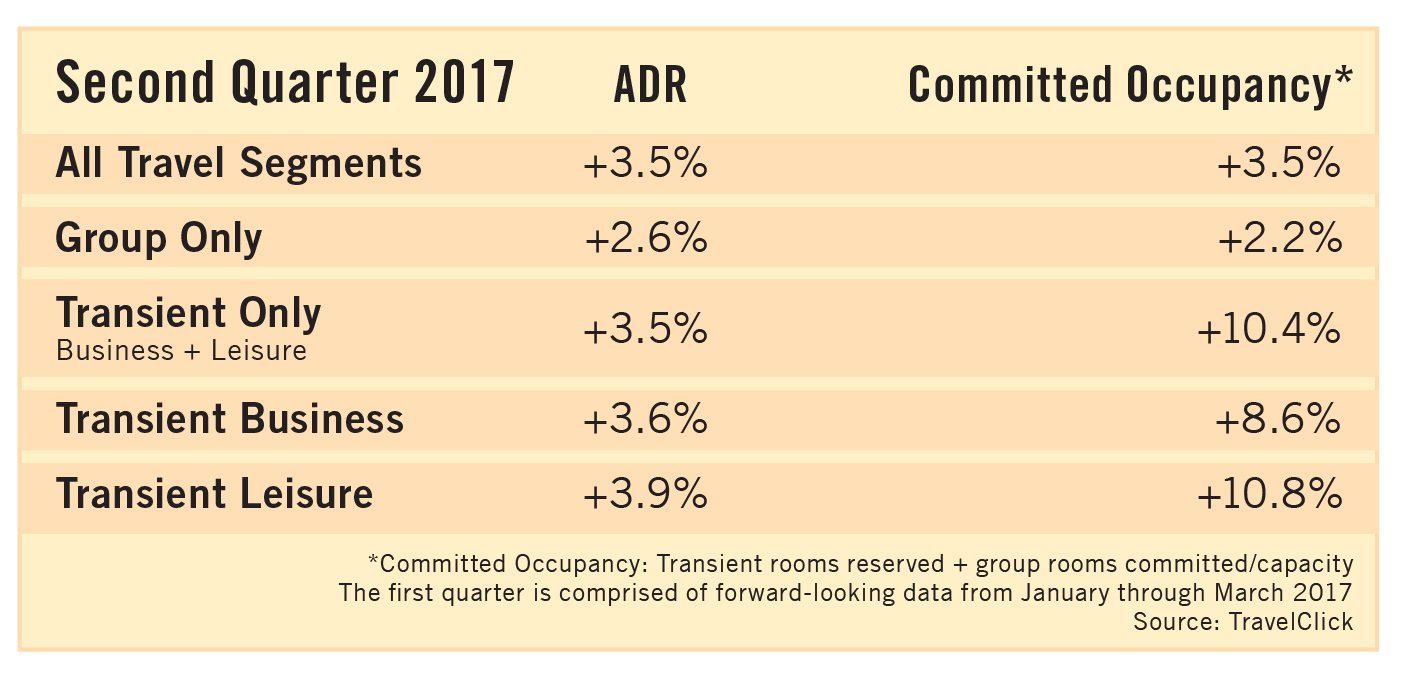

According to TravelClick’s January 2017 North American Hospitality Review, occupancy for the transient segment in particular is seeing significant growth in Q2, up 10.8% for transient leisure travel, 8.6% for transient business travel and 10.4% overall.

Hach agreed with the assessment that election-year uncertainty was a contributing factor to last year’s slow growth. “For most major companies, travel and entertainment is the second largest controllable expense, right after payroll. We did see in particular going into the latter months of 2016, into October and early November, that there was a suppression of new group booking pace,” he said.

And now? “We have seen an uptick in group. When group bookings coming into a market are relatively strong, hotels have more business that they realize will be coming into a local market, so they’re more apt to increase their transient rates, which definitely helps RevPAR,” said Hach. “With that said, what’s very interesting in 2017 is this is really proving to be a year of fragmented and sporadic demand. When we look at the business segment, we haven’t seen any prolonged uptick in business-negotiated rates. We do see stabilization in the slight increase in transient, but the balance there is that transient is really flowing into discounted leisure, rather than to say that the IBMs and Apples of the world are traveling more.”

What that means, he said, is that it’s more important than ever for hoteliers to look deeply into their local markets rather than across the board to the top 25 North American markets. “Back in 2014 and 2015, it was really that 80/20 rule where there were consistently 21 or 22 markets out of the top 25 that were showing positive growth,” said Hach, referring to the Pareto principle (or 80/20 rule) which states that for many events, roughly 80% of the effects come from 20% of the causes. “It’s much more important now for hoteliers to look deep into their local market, particularly into the group and corporate side, because that’s where we’re starting to see some of the uncertainty play out in certain markets.”

Hoteliers should also keep their eye on Q3. “When you go through April, May, June, we’re fairly optimistic about the growth. July, August, September is the most concerning quarter, and that’s really because of the group piece,” said Hach. “As for Q4 2017, there are early signs now that we’re going to close on a strong note. All of that is subject to change, but because group books so much further out than corporate transient, the second and fourth quarters look to be the most promising. The question that I really have and want to watch closely: How do we come down after the peak summer travel season? Right now, there is a lot of good demand pickup for April and May, and I think hoteliers should be very focused on their transient pricing for April and May because we’re starting to see good demand generation. Part of the question is if you take your trip earlier in the year, how will Q3 shape up?”

Hoteliers should also keep their eye on Q3. “When you go through April, May, June, we’re fairly optimistic about the growth. July, August, September is the most concerning quarter, and that’s really because of the group piece,” said Hach. “As for Q4 2017, there are early signs now that we’re going to close on a strong note. All of that is subject to change, but because group books so much further out than corporate transient, the second and fourth quarters look to be the most promising. The question that I really have and want to watch closely: How do we come down after the peak summer travel season? Right now, there is a lot of good demand pickup for April and May, and I think hoteliers should be very focused on their transient pricing for April and May because we’re starting to see good demand generation. Part of the question is if you take your trip earlier in the year, how will Q3 shape up?”

Another thing to look out for, Hach said, is the member-direct loyalty rates. “The brands are really trying to increase their loyalty enrollment…and I think that stimulates the opportunity to go, but the other piece it plays into a bit is the discounting strategies on the corporate-negotiated side. The hotel revenue managers want to make sure they’re keeping their corporate discounts in line now with their member-direct rates. Going into the later parts of 2017, that’s something we’re going to be watching very closely. Does that actually come back and put more pressure on those member discounts to stimulate local demand? That’s something to watch closely,” he said. HB